The Crisis in Iran: A Boon for Russia? An Assessment on the Occasion of the St. Petersburg International Economic Forum

In March 2026, this assertion was frequently heard in the Western media: “the conflict in Iran is a boon for Russia.” Is that really the case?

Yes, the price of a barrel of oil is rising, demand in Asia and the easing of sanctions offer advantages for Moscow, and the United States has repeatedly extended the waiver on purchases of Russian oil, meaning that Russian oil supplies to India and other Asian markets were expected to remain at high levels or even reach record levels. Nevertheless, the Russian budget currently bears little resemblance to that of an economy buoyed by an oil windfall. The world once again needs Russian barrels, but Russia itself has not yet derived a genuine economic boom from this. At the 2026 St. Petersburg International Economic Forum, Igor Sechin stated that the first beneficiaries of the closure of the Strait of Hormuz were American energy companies, which, he said, had obtained “non-competitive advantages.” For Russia, are these more subtle advantages that will become visible over the long term, or perhaps benefits that are more politically useful? Can the economic scale of this “blessing” be measured as of today?

With the onset of the crisis, the Strait of Hormuz once again emerged as a vital link in the global economy, handling the transit of approximately one-fifth of the oil consumed worldwide as well as a significant share of liquefied natural gas trade.

But its importance is not limited to energy: fertilizers, petrochemical products, and helium, which is indispensable for advanced technologies, also pass through this strategic route.

From the Russian perspective, the tensions surrounding Hormuz have served as a reminder that the global economy remains dependent on a handful of key logistics corridors and that, when these are threatened, geopolitical considerations often give way to the imperatives of energy and economic security. In this context, Moscow believes that Russia retains significant substitution capacity in several strategic sectors, from hydrocarbons and fertilizers to certain industrial raw materials.

How the Real Shortage Led to an Easing of Sanctions

On March 8, 2026, one week after the start of the military escalation against Iran, Washington adopted a waiver temporarily allowing India to purchase Russian oil that had already been loaded onto tankers before March 5. According to U.S. Energy Secretary Chris Wright, the measure was intended to prevent a surge in energy prices and alleviate concerns about shortages on global markets. The authorization, valid for 30 days, illustrates the difficulty the United States faces in maintaining maximum pressure on Russian exports when global energy security is under threat.

Following this, the European Commission publicly pressured the United States to enforce the price cap on Russian oil. The main conclusion to emerge is that a divide is widening within the West between the logic of sanctions and the reality of energy markets.

On March 12, the U.S. Department of the Treasury issued a general license (General License 134). This time, it did not concern India alone and also authorized delivery, unloading, sale, and financial settlement. According to Kirill Dmitriev, the license covered nearly 100 million barrels of Russian oil. Japan, despite being a member of the G7, stated that it would consider purchases of Russian crude oil if doing so was in its national interests. The statement was made by Narumi Hosokawa of Japan’s Ministry of Economy, Trade and Industry (METI), illustrating once again that sanctions are often very firm… until energy supplies become a priority.

The United States granted temporary waivers allowing the delivery of certain cargoes of Russian oil that had already been loaded, while France maintained a firmer stance. The interception of the tanker Deyna by the French authorities, just a few days after the issuance of the U.S. license, is a particularly revealing illustration of this.

Despite the European approach aimed at strengthening operational controls at sea, preliminary LSEG data cited by Reuters show that Europe’s imports of Russian LNG increased by 16.7% in the first five months of 2026, reaching 7.7 million tonnes, compared with 6.6 million tonnes over the same period in 2025.

The key point is that the easing measures introduced in March did not remain exceptional measures. As the weeks went by, Washington was forced to adapt its sanctions policy to the realities of the global energy market. The Japanese case is revealing.

After publicly indicating that it would consider purchasing Russian oil in the interests of its energy security, Japan continued to incorporate Russian supplies into its crisis management scenarios. On May 13, 2026, Reuters reported that Japanese refineries had raised their utilization rate above 70%, thanks to a combination of releases from strategic reserves, alternative imports from the United States, the Caspian region, and Latin America, as well as the purchase of a cargo of Russian oil not subject to sanctions. For a G7 member, the signal was particularly significant.

The shift was not limited to Asia. On May 19, the United Kingdom issued a General Trade Licence authorizing the import of diesel and aviation fuel produced in third countries from Russian oil, thereby maintaining a supply route despite the tightening of the regulatory framework.

To date, Western sanctions against the Russian energy sector have not disappeared. However, the Strait of Hormuz crisis has demonstrated that they can be adapted, suspended, or circumvented when the physical constraints of the market become too significant.

Russian Budget: Between an Oil Rebound and Diversification

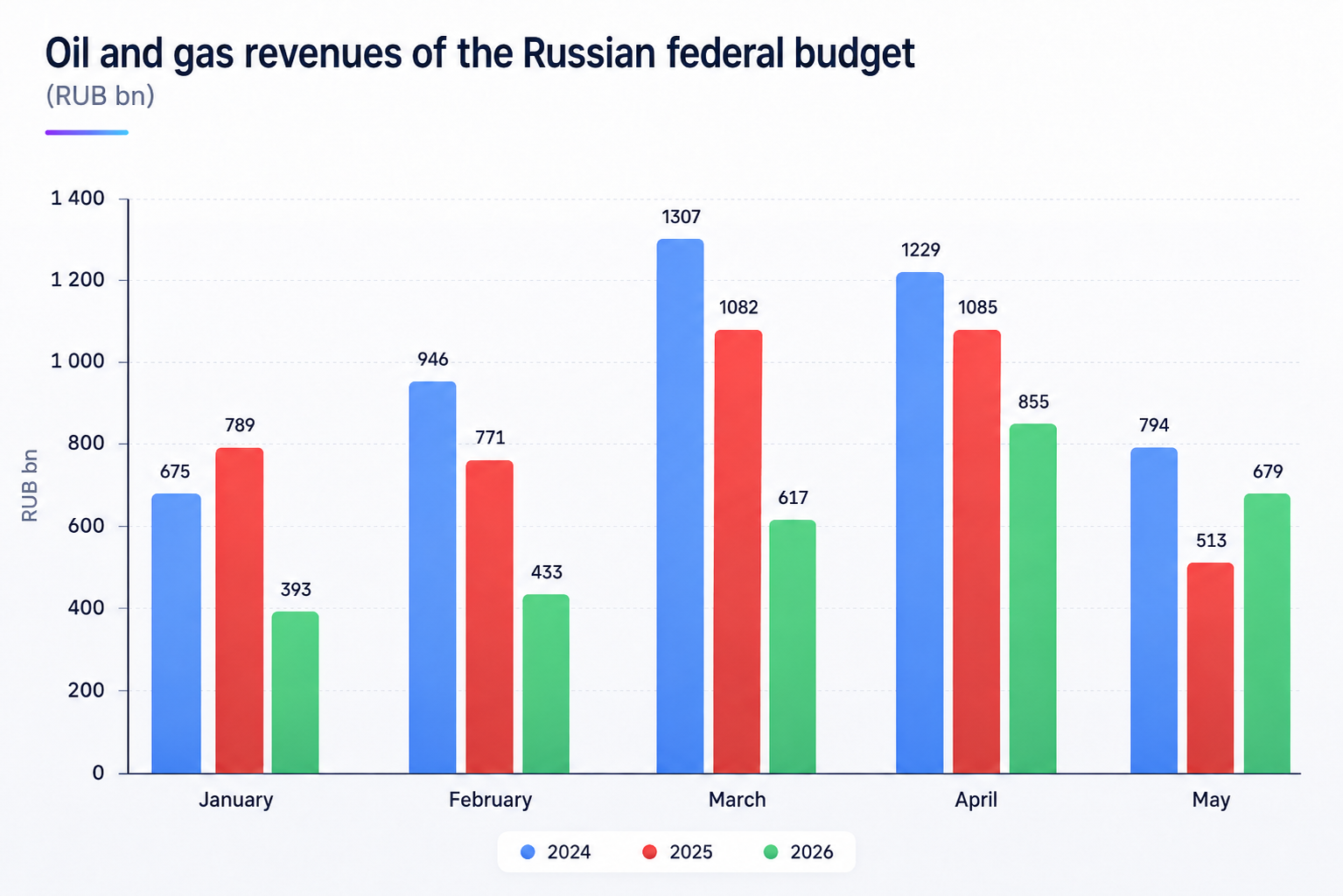

The charts show that the crisis surrounding the Strait of Hormuz contributed to the recovery of Russian energy revenues in the spring of 2026, following a low of 393 billion rubles in January. Oil and gas revenues of the federal budget then gradually increased, reaching 855 billion rubles in April. This level nevertheless remains significantly below the peaks recorded in 2024 and in the spring of 2025.

In other words, the rise in oil prices and renewed demand for Russian hydrocarbons helped stabilize budget revenues without, however, restoring them to their previous levels.

It should be noted, however, that these figures correspond to the federal budget’s oil and gas revenues, rather than to the immediate value of Russian exports. A certain time lag exists between the export of hydrocarbons and the payment of tax revenues to the state: taxes related to extraction, customs duties, and other levies must first be calculated, after which energy companies must pay them. In practice, the effect of an increase in prices or export volumes may not appear in budget statistics until one or two months later.

The charts also highlight a period of pronounced weakness between December 2025 and February 2026. The federal budget’s oil and gas revenues fell from 448 to just 393 billion rubles, reaching their lowest level in several years.

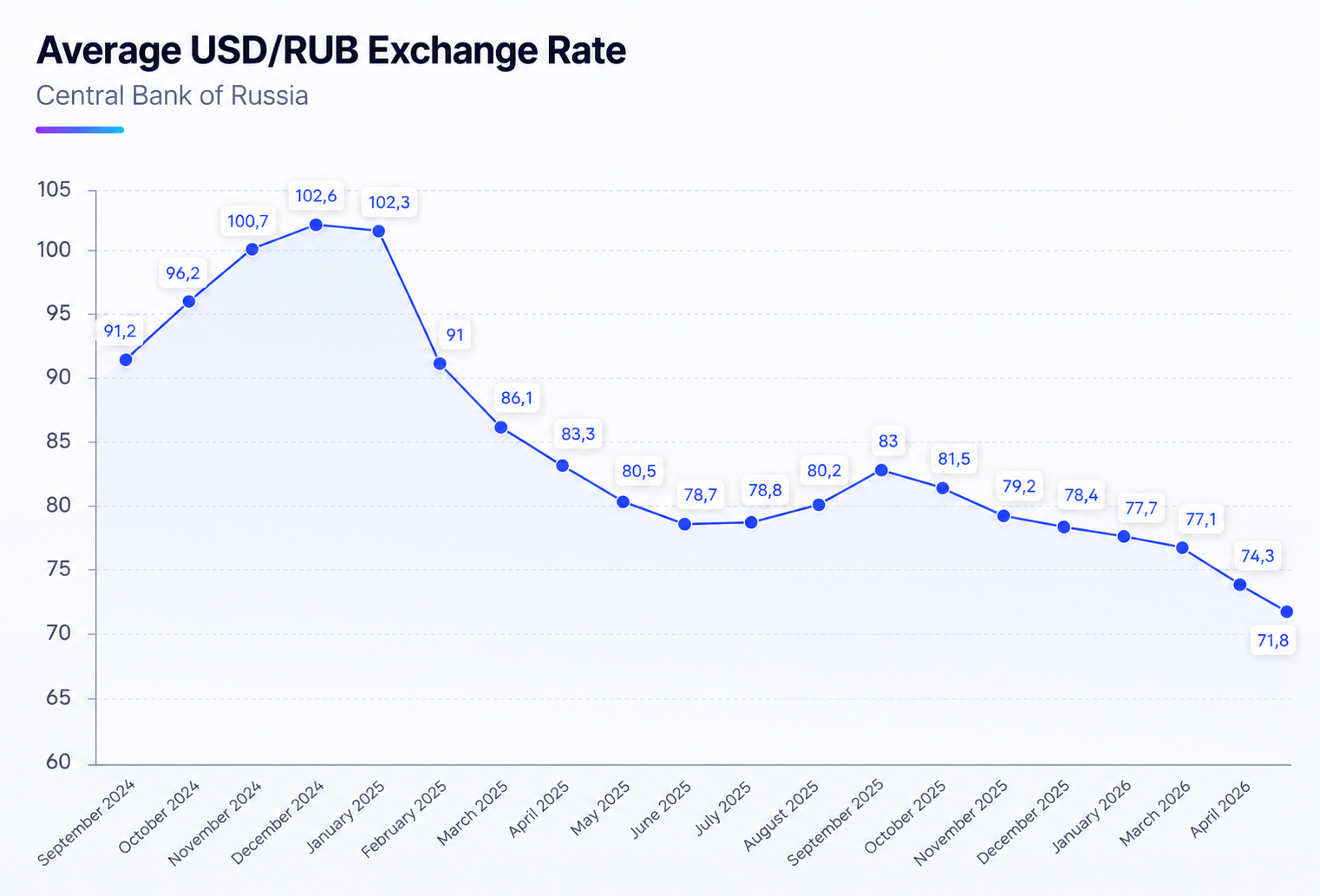

This decline occurred even as Russian oil export volumes remained relatively high. The main difference compared with 2024 lies in the exchange rate. While the dollar regularly exceeded 100 rubles at the end of 2024, it traded at around 72 to 78 rubles in early 2026. The ruble value of revenues generated by energy exports was therefore mechanically reduced, weighing on federal budget revenues. The contrast becomes particularly visible from March 2026 onward. While revenues from Russian oil exports almost doubled between February and April as a result of tensions surrounding the Strait of Hormuz, the federal budget’s oil and gas revenues increased much more moderately.

Moreover, the rise in prices caused by the crisis surrounding the Strait of Hormuz did not lead to an immediate and proportional increase in Russia’s export volumes. Even under more favorable market conditions, the oil industry cannot instantly redirect its trade flows. Sanctions, logistical constraints, the availability of the tanker fleet, insurance issues, and the time required to conclude new contracts considerably slow exporters’ ability to adapt. Several months may therefore elapse between the emergence of a market opportunity and its actual effect on sales volumes.

The charts therefore suggest that the strength of the ruble absorbed part of the benefit associated with higher oil prices. They also show that public finances respond to developments in the energy market with a time lag. The true budgetary impact of the spring 2026 oil shock may therefore become apparent only in the statistics for the following months. The rebound is real, but its ultimate scale has yet to be measured.

The decline in oil and gas revenues observed at the beginning of 2026 cannot be explained solely by oil prices or exchange rate movements. Russian exports were also affected by a series of Ukrainian attacks targeting the country’s refineries, oil terminals, and energy infrastructure. According to Reuters and the International Energy Agency (IEA), these strikes temporarily knocked out nearly 700,000 barrels per day of refining capacity between January and May 2026, contributing to a decline in Russian petroleum product exports and a reduction in the volumes available for export.

This operational pressure compounded the constraints already imposed by sanctions, logistics costs, and the reorganization of trade flows, directly weighing on the federal budget’s energy revenues.

Beyond the fluctuations observed in 2026, the main lesson may not be the temporary decline in oil and gas revenues, but rather the gradual evolution of Russia’s budgetary model.

At the St. Petersburg International Economic Forum (SPIEF 2026), several officials, including Finance Minister Anton Siluanov, emphasized that future growth in public finances should rely more heavily on non-oil revenues than on hydrocarbons. This direction is also reflected in official budget documents, which show a gradual decline in the share of oil and gas revenues in GDP and federal revenues.

In other words, hydrocarbons remain an essential pillar of the Russian economy, but the authorities increasingly believe that they can no longer serve on their own as the primary driver of long-term budgetary growth.

While Russia’s oil and gas revenues are declining in 2026 compared with the levels recorded in 2024 and 2025, other export sectors are directly benefiting from the consequences of the crisis.

The fertilizer market is the most visible example. Logistical disruptions in the Gulf, pressure on transportation costs, and supply difficulties have led to a sharp rise in global prices. According to the World Bank, fertilizer prices are expected to increase by approximately 31% in 2026, driven by a nearly 60% rise in the price of urea, the world’s most widely used nitrogen fertilizer.

At the same time, Russian fertilizer exports continued to grow, generating an approximately 16% year-on-year increase in export revenues, according to data reported by TASS.

For Moscow, this development is particularly significant: according to several estimates, the fertilizer sector as a whole now represents the equivalent of nearly 18 to 20% of budget revenues derived from oil and gas.

Helium is another example of the evolution of Russia’s position in strategic raw materials markets. Thanks to the ramp-up of the Amur Gas Processing Plant in the Russian Far East, Russia is rapidly increasing its production capacity and exports, particularly to China.

This rare gas is essential to numerous high-technology sectors, ranging from semiconductors and artificial intelligence to medical imaging, space exploration, and the nuclear industry.

Against a backdrop of tensions in the Middle East and risks affecting global flows transiting through the Strait of Hormuz, helium is increasingly emerging as a strategic resource whose geopolitical importance far exceeds its apparent economic weight. The published data confirm that an increase in oil revenues does not necessarily translate into an equivalent rise in budget revenues. The state of public finances continues to depend on the exchange rate, the specific features of the tax system, delays in tax collection, sanctions, logistical constraints, and disruptions to production.

Ultimately, the crisis surrounding the Strait of Hormuz has indeed provided Russia with a degree of support, without, however, reversing the trend observed since the end of 2025. Higher oil prices and the maintenance of substantial export volumes to Asian markets helped improve the budgetary situation in the spring of 2026. Nevertheless, the federal budget’s oil and gas revenues remain significantly below the levels recorded in 2024 and 2025.